The January 2019 news about declining employer taxes was stellar. The May 2019 financial report reveals that the trust fund is in even better shape: nearly $1.9 billion as of April 30th.

Note: of course, benefit payments continue their decline, dropping 6.7% from 2018 numbers to $330.9 million as of April 2019. Employer taxes are also down $23.9 million, to $330.9 million, for January to April 2019.

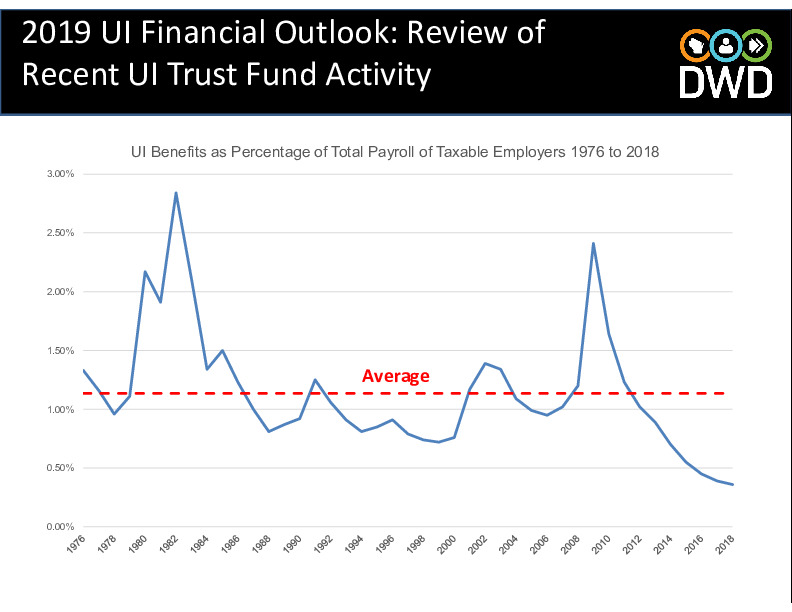

At the May 22nd meeting of the Advisory Council, there was a presentation on the health of the unemployment trust fund. An excellent chart in this presentation presents the current situation:

{kind=link}

As evident here, the trust fund is at a near record high while claimants’ benefits and employers’ taxes are dropping like rocks down the proverbial well. Two charts showcase how benefits and taxes have markedly declined since 2011 (benefits) and 2012 (taxes) relative to total payroll in the state.

So, what Wisconsin has experienced the last eight to nine years is ahistorical — only around 37% of claimants applying for unemployment benefits end up receiving any benefits rather than the more typical 55% of applicants.

Note: Department personnel continue to remark about how benefit payments are at record lows without offering any explanations or theories for why these record low benefit payments are occurring. As noted in this blog, this problem of record-low benefit payments is not unique to Wisconsin. But, it does seem from this same note that changes in how states are administering their unemployment law disqualifications are responsible for much if not all of this decline. Shouldn’t the Department finally take ownership of its own culpability for what has been going on the last eight to nine years or at least explain why the legal changes and administrative practices adopted under the prior governor to make it more difficult to claim unemployment benefits are somehow NOT connected to this decline in unemployment benefits?

At a minimum, Department staffers need to read Andrew Stettner’s excellent analysis of state unemployment systems and the changes in eligibility standards and application rates describes the impact of these changes and why these changes should be re-examined and most likely reversed.

To understand how healthy the unemployment trust fund actually is, three different scenarios for the future were played out in this presentation.

- In one scenario, the economy continues along its current course, benefit payments remain anemic, and the unemployment rate returns to the normal 4-5% for Wisconsin. Here, the trust fund continues to be robust in the short-term. But, growth of the fund eventually slows, and the fund begins to decline slightly in the long-term.

- In the second scenario, the economy continues along its current course, but benefit payments return to the historical experience of Wisconsin. While no recession is assumed to take place, the trust fund balance starts to take a hit in 2020 and a switch to the more aggressive tax schedule C will be needed by 2026 or so.

- In the third scenario, a mild recession in 2020 occurs. Even with the anemic level of benefit payments continuing — 37% — the bottom of the trust fund drops out such that less than $500 million is left in the fund by 2022. And, in the long-term, the most aggressive tax schedule — Schedule A — needs to be triggered to start pumping money back into the trust fund.

In other words, these scenarios indicate that the trust fund balance — despite being at record levels — is wholly inadequate given the current size and scope of Wisconsin’s economy. Only a Pollyanna desire for the economic equivalent of sunshine and rainbows to continue indefinitely keeps the unemployment trust fund from imploding.

The current fetish with minimizing employers’ taxes is just one culprit behind this carefree thinking. Economists have begun explaining, that there is no correlation whatsoever between employers’ tax rates and business success. What remains to be seen is what the Advisory Council will do about all these problems: keep current policies and administrative practices in place or begin the process of changing these policies and practices. As many of these simply relate to the Department’s bureaucratic preferences in how it administers unemployment law (and, in numerous places represents a sharp conflict with that law), there is much that can be done immediately to correct at least the unparalleled decline in benefit payments before we find ourselves in the middle of a recession and with no oar available to avoid the waterfall towards which we race.